How I Survived a Debt Crisis Without Losing My Mind — Cost Control Lessons the Hard Way

I used to think I was smart with money—until my debt started swallowing my paycheck whole. It crept up slowly: missed payments, high balances, constant stress. I felt trapped, like I was running in place. The anxiety was constant, the shame quiet but deep. But through trial, error, and some brutal lessons, I found ways to regain control. This isn’t a magic fix, but a real story of how cost control became my lifeline when the financial walls were closing in. It’s about what broke me, what rebuilt me, and how anyone can find their footing again—not through luck, but through deliberate choices.

The Breaking Point: When Debt Stops Being Manageable

There was no single moment that signaled the crisis—no dramatic event, no sudden job loss. Instead, it was a slow erosion, like water wearing down stone. At first, the credit card balances felt manageable. A few hundred here, a few hundred there—just temporary, I told myself. But over time, those small balances grew. Payments were delayed, then missed. Minimum payments became the norm, not the exception. Each month, the balance barely budged, while interest quietly compounded. What started as convenience became a chain.

The emotional toll was just as heavy as the financial one. I began checking my account balance with dread. Opening the mail felt like facing an enemy. Late notices piled up, not because I ignored them, but because I couldn’t face what they represented. There was a constant hum of anxiety in the background of daily life—a low-grade panic that made it hard to focus, to sleep, to enjoy even small pleasures. I felt isolated, convinced I was the only one struggling, even though I knew that couldn’t be true.

What made the situation worse was the illusion of stability. My income hadn’t dropped. My lifestyle hadn’t changed dramatically. Yet, the money disappeared. I wasn’t living extravagantly—no luxury vacations, no designer clothes. But the small leaks added up: subscription renewals I forgot to cancel, automatic payments for services I no longer used, dining out more than I realized. These weren’t reckless choices, but they were unconscious ones. And over time, they created a gap between what I earned and what I actually had.

The breaking point came when I tried to book a flight for a family event and discovered my card was declined. It wasn’t due to fraud or a technical error—it was simply over its limit. That moment shattered the illusion. I wasn’t just behind; I was drowning. And I realized that if I didn’t make a change, the cycle would only tighten. I wasn’t spending too much on luxuries—I was spending too much on autopilot. The crisis wasn’t about income; it was about control.

The Illusion of Control: Common Missteps in Early Damage Control

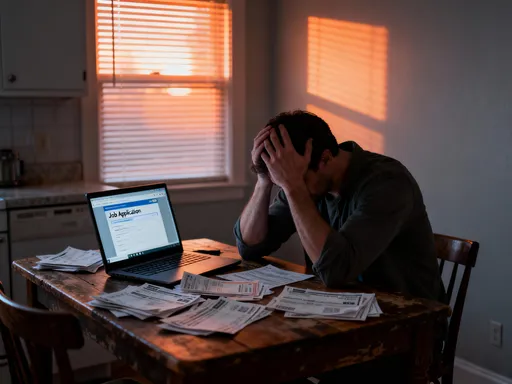

When the reality of the debt hit, my first instinct was to act—any action felt better than helplessness. I started cutting back immediately, canceling my gym membership, skipping my morning coffee, and cooking every meal at home. These changes felt productive, even virtuous. I told myself I was being disciplined. But within weeks, I was still falling behind. The truth was, I was focusing on the wrong things. I was making symbolic cuts while ignoring the real drivers of my financial strain.

One of the biggest mistakes I made was shifting debt from one card to another using balance transfer offers. It seemed like a smart move—lower interest, temporary relief. But I didn’t stop using the original card. I treated the newly freed-up credit as extra spending room, not as a tool for repayment. The result? I now had two cards carrying balances, and when the introductory rate expired, the interest rate jumped. What felt like a solution became another trap. I had confused moving debt with eliminating it.

Another common misstep was paying only the minimum on all accounts. It kept me in good standing with creditors, so I thought I was doing enough. But I didn’t fully understand how interest worked. On a $5,000 balance at 18% APR, paying only the minimum could mean decades of payments and thousands in interest. I was barely covering the interest, let alone reducing the principal. I was staying afloat, but I wasn’t moving forward. The minimum payment wasn’t a strategy—it was a delay tactic.

I also made the error of cutting essential spending to fund non-priorities. I stopped filling my prescription to save money, only to end up paying more later in medical costs. I let my car insurance lapse to free up cash, increasing my risk of a catastrophic financial hit if I were in an accident. These decisions were born of desperation, not strategy. They gave me temporary relief but created long-term vulnerabilities. I was solving for today at the expense of tomorrow. Real financial recovery requires trade-offs, but not reckless ones.

Rethinking Cost Control: From Cutting Coffee to Strategic Reduction

True cost control isn’t about deprivation—it’s about intentionality. I learned that the difference between surviving and progressing wasn’t how much I cut, but how I cut. The viral advice about skipping your daily latte might save you $5 a day, but if your cable bill is $120 a month and you barely watch TV, that’s where the real opportunity lies. I shifted my focus from small, visible expenses to larger, less obvious ones—the financial leaks that go unnoticed because they’re automated or normalized.

One of the most effective changes I made was renegotiating recurring bills. I called my internet provider and asked for a better rate. I was ready to switch, but they offered a discount to keep me. That single call saved me $30 a month—more than a year of skipped coffees. I did the same with my phone plan, my insurance, even my utility provider. These weren’t one-time wins—they were sustainable reductions. Unlike cutting out coffee, which felt like a loss, this felt like empowerment. I wasn’t giving up anything; I was claiming value I was already entitled to.

I also took a hard look at subscriptions. I had signed up for services during promotions, forgotten about them, and let them renew automatically. Streaming platforms, meal kits, cloud storage, fitness apps—the list was long. I reviewed every charge on my statements and canceled what I didn’t use regularly. That freed up over $70 a month. More importantly, it taught me to question every automatic payment. Just because it’s convenient doesn’t mean it’s necessary. I started treating subscriptions like appointments—if I didn’t show up, I shouldn’t pay.

Strategic reduction also meant rethinking how I used what I already had. Instead of buying new tools for a home project, I borrowed from a neighbor. Instead of eating out on weekends, I planned meals in advance and cooked in batches. These weren’t about living with less—they were about using resources more efficiently. I stopped seeing cost control as a punishment and started seeing it as a form of financial fitness. It wasn’t about what I couldn’t have; it was about making my money work harder for me.

The Cash Flow Fix: Aligning Income, Expenses, and Debt Payments

One of the biggest blind spots in my financial life was cash flow. I knew my salary, and I knew my bills, but I didn’t know how they lined up over the month. I was paid biweekly, but most of my bills were due in the first week of the month. That meant I had a cash crunch every few weeks—even though I earned enough to cover everything. I was technically solvent, but I felt broke because the timing was off. Fixing this wasn’t about earning more—it was about aligning what came in with what went out.

I started by mapping my income and expenses on a calendar. I marked every payday and every due date. The pattern was clear: I had two paychecks, but three major bills due within five days of each other. That created a bottleneck. To fix it, I contacted my utility provider, my internet company, and my insurance carrier to adjust billing dates. I moved some payments to the second paycheck of the month. That simple change eliminated the monthly crunch. I wasn’t spending less, but I was managing better.

I also began tracking every dollar I spent for 30 days. I used a simple spreadsheet, but apps can work too. The goal wasn’t perfection—it was awareness. I discovered that small, irregular expenses—gas, groceries, pharmacy runs—added up to over $400 a month. That was more than my car payment. Without tracking, those expenses were invisible. With tracking, I could plan for them. I started setting aside money weekly, not just for fixed bills, but for variable ones too. That turned surprises into expectations.

Another key step was creating a payment hierarchy. I decided what got paid first: essentials like rent, utilities, and minimum debt payments. Then I allocated extra funds to high-interest debt. This wasn’t rigid—life happens—but having a plan meant I wasn’t reacting in panic. I also set up automatic transfers to a separate account for irregular expenses. Every payday, $50 went into that account. It wasn’t much, but it built up over time and prevented overdrafts when unexpected costs came up. Cash flow isn’t glamorous, but it’s the foundation of financial stability.

Debt Strategy That Actually Works: Beyond Minimum Payments

Once I had a clearer picture of my cash flow, I could focus on getting out of debt—not just managing it. I moved beyond minimum payments and adopted a real repayment strategy. I evaluated two popular methods: the debt avalanche and the debt snowball. The avalanche method focuses on paying off debts with the highest interest rates first, which saves the most money over time. The snowball method targets the smallest balances first, which builds momentum through quick wins. I chose a hybrid approach—one that balanced math with motivation.

I started by listing all my debts: credit cards, medical bills, a personal loan. I noted the balance, interest rate, and minimum payment for each. Then I sorted them by interest rate. The highest was a credit card at 22.99%. That should have been my first target. But I also had a $300 medical bill at 0% interest—small, but a constant reminder of my stress. I decided to pay that off first. It wasn’t the most efficient move, but it gave me a psychological win. Clearing that balance made me feel capable, which made it easier to tackle the bigger ones.

After that, I switched to the avalanche method. I threw every extra dollar at the 22.99% card while making minimum payments on the others. I calculated that by adding just $100 a month beyond the minimum, I could save over $1,200 in interest and cut the payoff time by more than half. That number kept me focused. I wasn’t just making payments—I was reclaiming money that would have gone to interest.

I also considered consolidation. A balance transfer card with a 0% intro rate could have helped, but I was cautious. I’d been burned before by temporary fixes. I applied only after I had a solid budget and a plan to avoid new charges. When approved, I transferred the high-interest balance and committed to paying it off within the intro period. I froze the old card and didn’t close it—to protect my credit history. Consolidation isn’t a solution on its own, but when combined with discipline, it can be a powerful tool. The key is to treat it as a bridge, not an escape.

Building a Buffer: Why Emergency Savings Matter Even in Crisis

One of the most counterintuitive lessons I learned was that saving and debt repayment aren’t enemies—they’re allies. I used to think I couldn’t save until I was debt-free. But every time an unexpected expense hit—a flat tire, a vet bill, a broken appliance—I had to put it on a credit card. That meant I was taking one step forward and two steps back. I realized I needed a buffer, no matter how small, to protect my progress.

I started with $20 a month. It felt pointless at first—barely enough for a tank of gas. But I treated it as non-negotiable, like a debt payment. After six months, I had $120. Then I raised it to $50. Over time, I built a $1,000 emergency fund. That may not sound like much, but it covered most of the small crises that used to derail me. When my washing machine broke, I paid for repairs without touching my credit card. When my daughter needed new glasses, I didn’t panic. The buffer didn’t prevent problems, but it prevented debt relapses.

I kept this fund in a separate savings account, not linked to my debit card. That made it harder to dip into casually. I also set a rule: it was only for true emergencies—not for shopping, not for vacations, not for convenience. This fund wasn’t about wealth—it was about stability. It gave me breathing room. I no longer had to choose between fixing my car and paying my rent. That single $1,000 buffer reduced my anxiety more than any other financial change.

Experts often say you need three to six months of expenses saved, but that goal felt impossible when I was in crisis. I focused instead on progress, not perfection. I celebrated every $100 milestone. I reminded myself that a small buffer is better than none. And I learned that saving isn’t a luxury for the debt-free—it’s a necessity for anyone trying to get there. It’s not about how much you save; it’s about making saving a habit, even when it feels impossible.

Staying the Course: Habits, Triggers, and Long-Term Stability

Getting out of debt wasn’t the end—it was the beginning of a new phase. The real challenge wasn’t the payoff; it was staying out. I had to rebuild not just my balance sheet, but my relationship with money. That meant understanding my triggers—the emotions, situations, or habits that led me to overspend. For me, stress was a major one. When I felt overwhelmed, I used shopping as a distraction. Boredom was another. I’d browse online stores just to pass the time, and end up buying things I didn’t need.

I started by identifying my spending patterns. I reviewed my statements monthly and looked for trends. I noticed that most of my impulse purchases happened on weekends, often after scrolling through social media. I also spent more when I was tired or emotionally drained. Awareness was the first step. Then I built systems to protect myself. I unsubscribed from marketing emails. I deleted shopping apps from my phone. I set a 24-hour rule for any non-essential purchase. These weren’t restrictions—they were safeguards.

I also created positive financial habits. I scheduled a weekly money check-in—15 minutes to review spending, track progress, and adjust as needed. I used visual tools, like a debt payoff chart, to see how far I’d come. Celebrating small wins kept me motivated. Paying off a credit card wasn’t just a transaction—it was a victory. I shared those wins with my family, not for praise, but to reinforce the behavior.

Long-term stability isn’t about never making mistakes—it’s about having systems that catch them. I still have months where I overspend. But now, I have a budget to return to, a buffer to fall back on, and habits that guide me back on track. Financial peace isn’t a destination; it’s a practice. It’s built not in grand gestures, but in daily choices. I didn’t survive the debt crisis because I became perfect. I survived because I became consistent. And that’s something anyone can do.